There’s a danger few in Westminster are willing to say out loud. Britain is at risk of becoming a US talent depot in the emerging age of artificial intelligence - a nation that trains the minds, but not the companies, of the future.

The resource being extracted isn’t oil or minerals. It doesn’t lie under our soil; it walks our campuses, codes in our labs, and defends theses in our universities, before boarding flights to California.

In the twentieth century, the United States built its strength on other nations’ resources: immigrants from around the world, Saudi oil, Latin American minerals, Asian manufacturing. In the twenty-first, it is building on other nations’ minds. And Britain, with its world-class universities, English language, and open flow of skilled graduates, has become the best place to draw from. The UK comprises around just 0.84% of the global population, yet 17% of the top universities (QS 2026) are based in the UK, with 4 being in the top 10.

These universities have been quick to support high quality technology-related courses at remarkable scales. In 2022 the UK graduated around 46,000 students from AI-related programmes - more than any other country in Europe – with Germany second at 32,000. That should be the foundation of a domestic AI industry. Instead, it risks becoming our next great export.

Speak to the people inside that number - a PhD student in Edinburgh, an engineer in London, a computer science undergraduate in Cambridge - and the pattern repeats. They are applying for American scholarships, raising venture capital from Silicon Valley, or accepting job offers that pay twice as much abroad. Britain is helping to producing the intellectual fuel for the AI revolution, while others build the engines that run on it.

The Upside - and the Depot Risk

On one level, the influx of US tech capital into the UK is unquestionably welcome. For example, Microsoft Corporation has announced a US $30 billion (≈£22 billion) investment in the UK between 2025-28, including $15 billion of capital expenditure to build cloud and AI infrastructure and a UK-based supercomputer with more than 23,000 GPUs.

Similarly, US-tech firms under the UK-US “Tech Prosperity Deal” have pledged around £150 billion over 10 years – a titanic sum given the size of the UK economy.

And Palantir has signed a UK-government deal to invest up to £1.5 billion and base its European defence-HQ in London, creating up to 350 high-skill jobs and mentoring UK SMEs.

But there is a deeper dimension. This capital and infrastructure will help US firms access British talent, British compute, and British data-centres - and use them as bases for global operations. The UK is providing the raw inputs; the US firms are providing the strategic architecture and capturing the value. In effect, Britain is acting as a talent and infrastructure depot for US innovation - not building/scaling its own companies, its own AI brands, or taking the lion’s share of value-capture within its borders.

For the UK to break free from its role as an extraction hub, the path forward is clear. Talent must not only be cultivated domestically, but the enterprises it creates must be anchored here - with intellectual property, corporate headquarters, and profits retained onshore. Without this, such investments reinforce dependence rather than build independence.

Why the US Keeps Winning the Talent Game

1. Terrible Incentive Structures

The gravitational pull of American pay is hard to overstate. A mid-career AI engineer in the United States can expect total annual compensation of around $240,000 (roughly £190,000) according to Levels.fyi’s global dataset. In London, the typical range for comparable roles is closer to £75,000–£95,000. Outliers at major tech firms and hedge funds exist, but the averages tell the story of 50% cheaper talent, for talent at universities of comparable quality.

Things are worse at the startup level. Under the Qualified Small Business Stock (QSBS) regime, founders and early employees can sell up to $10 million worth of startup shares free of federal tax. This has now increased to $15 million as of July. The UK is going in the other direction. Entrepreneurs pay a reduced tax rate (10%) on the sale of their business or shares, but only on the first £1 million of lifetime gains. From April 2025 that rate rose to 14%, making the scheme laughable compared to US rates.

Over time these differences shape where talent concentrates. Bright engineers and researchers don’t just cross the Atlantic for a bigger pay cheque; they move because the upside of success - the ability to take a shot and keep the reward - is structurally greater. Britain ends up training the talent, but America captures the entrepreneurs.

2. The Capital Gap

Even if pay were competitive, money builds ecosystems, and almost all the money is in the United States. In 2024, about three-quarters of all private AI investment worldwide flowed there - roughly $109 billion, compared with around $4.5 billion in the UK, according to the Stanford AI Index. That disparity doesn’t just look bad in a chart; it decides who gets to rent the next generation of AI chips, hire teams at scale, and reach global markets first.

For British founders, the path to serious growth capital still runs through San Francisco. The result is predictable: headquarters shift, intellectual property migrates, and the UK becomes the R&D wing of the US, Japan etc.

If Britain cannot close the gap in both pay and capital, it will continue to play the same role in the AI economy that it once did in manufacturing: providing skilled labour and ideas, while others build the giants that go on to create substantial long-term value.

3. The Compute Gap

AI runs on computing power - supercomputers stacked with specialist processors that train and run models. These are the new oil refineries.

The UK is making progress. Isambard-AI in Bristol and Dawn in Cambridge, both part of the new AI Research Resource (AIRR), are major steps forward. Microsoft has pledged to bring 20,000 advanced chips to UK data centres by 2026. But the world’s biggest and most flexible clusters remain in the US. British startups looking for large-scale computing still find the best access on the West Coast.

4. Uncompetitive Energy Prices

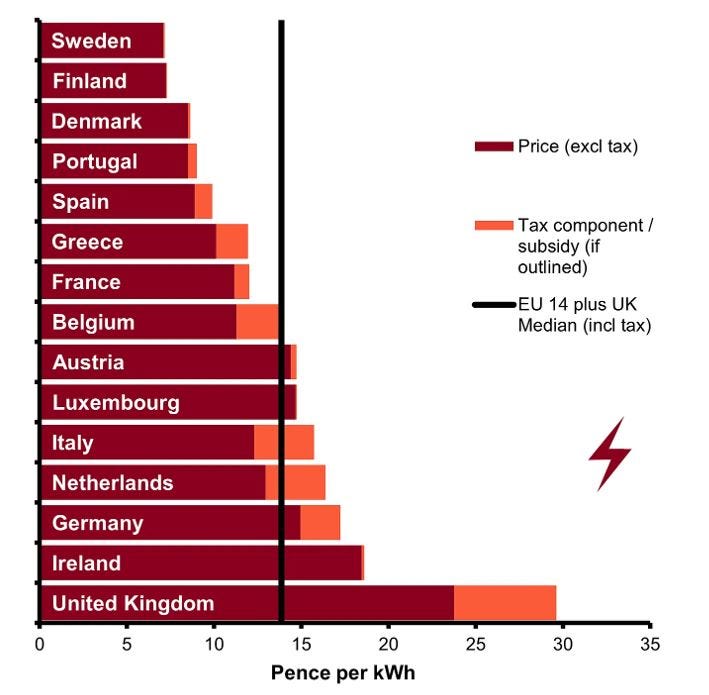

It is no secret now that energy requirements for AI is extensive. Training and running modern models consume vast amounts of power. Modelled estimates suggest emissions stemming from AI will surpass all global aviation emissions. This is why China has been accelerated all forms of energy generation in preparation for this future. Britain’s industrial electricity prices are twice the EU average (Figure 1), making them the highest in Europe, and far above those in the US. Every company training models here pays a built-in premium that has been labelled as commercial unviable for many startups and companies. It is the cost of energy that makes the US tech investment dubious. Energy prices will have come down dramatically in the next 5 years if the UK is to see more firms like Graphcore or Synthesia, or another DeepMind or Oxford Ionics, purchased by Google and IonQ respectively.

Figure 1. Average Industrial Electricity Prices (kWh) for the UK and 14 EU countries, measured by the medium consumer in late 2024 (Turner 2024).

5. Visa Structure

The UK attracts tens of thousands of international students into AI-related degrees each year - but too many leave after graduation. Proposals to shorten the post-study visa from two years to eighteen months send exactly the wrong message.

Meanwhile, US firms offer relocation packages and handle all visa bureaucracy. Britain pays to train talent, then waves it goodbye.

Wasted Human Capital

Being acquired by US giants is not inherently a bad thing - it provides access to capital and resources, but it also means the UK loses geopolitical leverage and autonomy in the decisions that will define the future. It increases the likelihood of fewer UK-listed public companies, which means less corporate activity and ultimately less tax revenue flowing directly to the UK. While US subsidiaries of these firms may still pay some UK taxes on their local operations, the bulk of profits, intellectual property, and strategic decision-making often shift offshore. This typically results in lower overall tax receipts, fewer high-value headquarters jobs, and less reinvestment in the domestic ecosystem.

The UK workforce will remain at the whims of the US giants. Layoff rounds can be distributed abroad to countries like the UK, when needing to downsize while avoiding domestic criticisms in the US.

Above all, what’s missing is real power over decisions that will shape the next decade and beyond.

None of the world’s top 25 companies (by market cap) are headquartered in Europe as of mid-2025, and certainly none of the new technology behemoths.

Consider AstraZeneca: it played a major role during the Covid-19 pandemic, yet today the UK has no emerging tech company capable of playing a similarly outsized role in the future. Worse still, AstraZeneca is moving closer to the US capital markets. In September 2025, the company announced plans to undertake a direct listing on the New York Stock Exchange, tapping U.S. investor depth while maintaining its UK listing and headquarters in Cambridge.

Without such anchor institutions staying and growing at home, with headquarters, intellectual property, high-value jobs and decision-making remaining local, investments risk reinforcing dependence rather than creating genuine independence.

The UK has done the hard work: world-class universities, a deep graduate pipeline, English speaking, and access to one of the world’s economic powerhouse cities - London. Yet instead of compounding those advantages, the country’s setbacks we discussed collectively smother innovation. Left unchecked, the cycle is simple. Britain trains the talent. The talent leaves or is under external leadership. The ecosystem loses density. Fewer mentors remain to train the next generation. That is what the road to becoming a talent petrostate could be: exporting the raw resource, importing the finished goods.

Possible Solutions

1. Make Compute Abundant and Predictable

Computing power is oxygen for AI. Without it, start-ups suffocate or emigrate. The UK must treat computing as national infrastructure, not an academic luxury.

That means scaling public supercomputers and opening them to businesses as well as researchers. Publish clear prices and allocation schedules so start-ups can plan. Integrate compute credits into every innovation grant. Streamline planning for new data centres and tie their electricity supply to stable, (ideally but should not overshadow cost) low-carbon baseload power.

2. Attack the Electricity Delta

AI is an energy-intensive business. At the current absurd energy prices, the UK can never hope to compete with Europe let alone the US and China. The UK cannot outcompete America’s cheap hydro and gas overnight, but it can narrow the gap.

Accelerate investment in renewables and nuclear to provide predictable low-cost baseload power. Offer targeted tax reliefs for data centres and AI computing clusters until those costs fall. This is not about permanent subsidies. It is about bridging a structural disadvantage so British firms can compete fairly.

3. Match the Equity Upside

People follow opportunity. The US system rewards risk with life-changing outcomes. Britain’s current rules cap ambition.

Raise the lifetime limit on tax-relieved share sales, restore the 10% rate for qualifying disposals, and modernise employee share schemes to allow meaningful ownership without bureaucracy. The message should be clear: if you build in Britain, you can win in Britain.

4. Fund the Scale, Not Just the Seed

Britain is good at starting companies but poor at scaling them. Angel investors and early-stage schemes are active, but the large, late-stage funds that turn start-ups into global players are mostly American.

The UK should direct pension funds and sovereign-style capital pools into domestic growth funds focused on technology. It should back homegrown vehicles capable of writing £50–100 million cheques and leading major rounds. Without that, the UK will continue to incubate companies that mature elsewhere.

5. Make “Stay” the Default

The UK trains tens of thousands of international students in AI, computer science, and data. The easiest way to build a dense ecosystem is to keep them.

Keep post-study visas generous and predictable. Create elite fellowship programmes that tie top graduates to British research labs and start-ups for five to ten years. Retaining trained talent is cheaper (and faster) than trying to lure it back later.

The Choice in Front of Britain

Talk to ambitious young people in the UK and you’ll hear the same refrain: “I’ll raise money in the US, incorporate there, or just move.” Why? Because pay is higher, upside is higher, capital is deeper, computing is cheaper, and energy is affordable.

None of that is destiny. The UK already has the biggest talent pool in Europe, the right language, and a global financial hub. The question is whether it uses those advantages to build its own ecosystem or to fuel someone else’s.

Do nothing, and Britain becomes Saudi Arabia in the AI age: exporting raw human talent, importing refined technology. Act decisively, and it becomes the refinery itself - turning knowledge into products, jobs, and influence.

Progressing will be slow and certainly woke make headlines, but it will decide whether the UK builds the future or merely supplies it.

References

Dealroom (2024) Global AI Funding Report 2024. Dealroom.co.

Department for Science, Innovation and Technology (2024) AI Opportunities Action Plan. London: GOV.UK.

Department for Science, Innovation and Technology (2025) New strategic partnership to unlock billions and boost military AI and innovation. London: GOV.UK.

Edwards, C. and Race, M. (2025) US firms pledge £150bn investment in UK as tech deal signed. BBC News, 17 September 2025. London: British Broadcasting Corporation.

The Quantum Insider (2025) UK and US seal tech pact with £31 billion AI and quantum push. London: The Quantum Insider.

Frost Brown Todd LLP (2024) Qualified Small Business Stock (QSBS) Overview. Available at: https://frostbrowntodd.com

Greenberg Traurig LLP (2024) QSBS Tax Treatment and Upcoming Changes. Available at: https://gtlaw.com

IT Pro (2024) Microsoft to Invest £2.5bn in UK AI Infrastructure. ITPro.com.

Levels.fyi (2024) Global Compensation Data for Machine Learning Engineers. Available at:

https://levels.fyi

Office for National Statistics (2024) UK Industrial Electricity Prices. London: ONS.

UK Research and Innovation (2024) AI Research Resource (AIRR) Programme Overview. UKRI.gov.uk.